From Monoliths to Ecosystems

The new R&D paradigm

Lavinia Woodward, Director, Client Advisory and Consulting, Excelra

Pharmaceutical R&D has transformed from vertically integrated companies to collaborative ecosystems. With biotechs generating over half of new drug approvals, AI democratising capabilities, and networks replacing traditional partnerships, biopharma must adapt. Success requires orchestrating multi-directional collaborations, leveraging data sovereignty, and building flexible models to thrive in the ecosystem era.

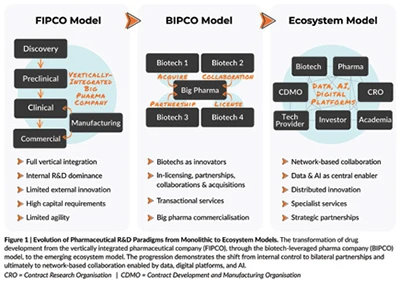

Historically, pharmaceutical innovation was concentrated among a small number of large companies. Believing control guaranteed success, the focus was on vertical integration, full spectrum ownership from discovery to development to commercialisation. However, escalating risk, spiralling R&D costs, compressed asset life cycles, increasing competitive intensity, and looming expiry of major patents, compounded by declining R&D productivity, and shifting geopolitical and regulatory landscapes, have driven fundamental changes to the drug development landscape.

Instead of traditional stakeholders dominating R&D, over half the drugs approved by the FDA in the last five years originate from small biotechs. Big pharma, having largely abandoned internal discovery, now buys innovation rather than creates it — a tacit admission that the old R&D paradigm has failed. Drug discovery has shifted away from a predominantly in-house process to an increasingly externalised one. Consequently, the business model prevailing among leading pharmaceutical companies, is the biotech-leveraged pharma company (BIPCO).

The BIPCO model has produced major scientific breakthroughs. To the benefit of millions of patients, advances in technology and the rise of the biotech sector have enabled the development of new, innovative, targeted therapies. However, we are already seeing a new trend emerge: the lessening dependency on big pharma partners to achieve regulatory success. What will become of the BIPCO?

Market dynamics, increasingly complex modalities, and the advancement of AI and digital technologies are reshaping pharma. There has been a transformation away from large, siloed companies to a multidisciplinary and data-driven approach to R&D. Biopharma leaders must tailor their business and operating models to this new R&D paradigm, or face irrelevance by 2030.

This article examines the pharmaceutical industry's evolution from the fully integrated pharmaceutical company (FIPCO) to today's emerging ecosystem model, exploring enabling factors behind the growing biotech independence, the role of networks and platforms in modern R&D, and technological forces democratising drug development. Most importantly, it provides strategic guidance for thriving in this new paradigm.

The Loss of Big Pharma's R&D Monopoly

As shown in figure 1, the biopharma landscape has fundamentally shifted, with the FIPCO business model transforming into an increasingly collaborative approach to R&D. In 2014, big pharma accounted for 72 per cent of the industry's R&D output; by 2023, it was 40 per cent. Large pharma’s internal R&D is no longer the primary engine of innovation. Instead, over half of late-stage pipeline assets are now externally sourced, originating from smaller biotechs.

The BIPCO model has enabled a striking geographic evolution. Chinese biotechs now supply 28 per cent of large pharma's in-licensed new drugs, up from single digits a decade ago. The growing role of China in big pharma’s R&D strategy is evidenced in recent mega-deals. In June of this year, AstraZeneca entered a strategic research collaboration with China's CSPC Pharmaceutical for US$ 100 million upfront with up to US$ 5.22 billion in milestones. This hefty sum provides the pharma giant access to CSPC’s AI-driven drug discovery platform. One month later, Pfizer committed US$ 1.25 billion upfront and up to US$ 4.8 billion in milestones for ex-China rights to 3SBio’s SSGJ-707, a bispecific antibody targeting PD-1 and VEGF developed using 3SBio’s proprietary CLF2 platform. Far outpacing global market growth, Chinese biopharma licensing deal value has increased 18-fold, from US$ 3.1 billion in 2015 to US$ 57.1 billion in 2024. No longer seen as the manufacturer of biosimilars, China has positioned itself as a powerhouse of R&D innovation.

The implications extend beyond individual transactions. Patent cliffs approaching in 2030 will see 190 drugs lose exclusivity, including 69 blockbusters, representing US$ 236 billion in sales at risk. According to Deloitte, the proportion of forecast late-stage pipeline revenue from in-house sourced assets is just over 50 per cent, confirming that external innovation has become essential rather than supplementary to big pharma's survival strategy.

Growing independence in the biotech sector

FDA approval data reveals biotechs achieving regulatory success with decreasing reliance on big pharma. Between 2023 and 2024, the proportion of FDA approvals that were sponsored or co-sponsored by companies generating over US$ 3 billion in revenue dropped from 63 per cent to 42 per cent. Indeed, the first eight and last twelve drugs approved in 2024 came from developers like Ligand, Idorsia, Betta, and Mesoblast - companies considered less-than-household names. In 2023, Pfizer gained seven approvals; in 2024, no companies scored more than two.

Approximately 60 per cent of biotech pipeline assets remain unpartnered; several important factors are enabling this autonomy:

• CROs offer comprehensive development services with regulatory expertise rivalling pharmaceutical companies

• Digital platforms enable global patient recruitment without established site networks and provide site selection support

• CDMOs provide immediate access to GMP-compliant manufacturing globally

• Alternative funding sources, including specialist investors and royalty financing, provide late-stage development capital

• AI and data platforms provide target identification, molecular design, protocol generation, patient matching, safety monitoring, regulatory intelligence, and predictive analytics through external providers

These developments provide small biotechs with the necessary capabilities for commercialisation without traditional big pharma partnerships. Meanwhile, larger biopharma companies can leverage the services of specialist providers to bolster tech capabilities, improve agility, and adapt to increasingly complex manufacturing requirements.

Networks as the New Operating Model

Almost half of pharma companies now outsource commercial capabilities, supporting accelerated adoption of external technologies. Thus, the R&D landscape is transforming into a complex network of interdependent specialists, where value creation depends not on vertical integration but on orchestrating multi-directional collaborations across specialised partners, each contributing distinct capabilities that no single company could efficiently replicate internally. CROs offer strategic partnerships beyond traditional exchange of services, technology companies provide the AI embedded throughout R&D platforms, academic institutions facilitate pre-competitive collaboration, and manufacturing networks ensure flexible, distributed production capacity.

These networks function differently from bilateral partnerships. Platforms like TransCelerate BioPharma demonstrate how shared infrastructure benefits multiple participants simultaneously. Founded in 2012, this nonprofit unites 20+ leading biopharma companies including AbbVie, Amgen, AstraZeneca, and GSK. Rather than each company building proprietary systems, TransCelerate has developed 570+ tools and resources accessible across the network. Their DataCelerate® platform enables secure sharing of de-identified data from over 85,000 patients across 130 studies, whilst their Digital Data Flow initiative transforms protocol digitalisation industry wide. The impact is tangible, with Amgen's Narimon Honarpour confirming that "TransCelerate has changed how we work as a company". This model demonstrates how tomorrow's competitive advantage comes not from owning infrastructure, but from orchestrating collaborative networks that benefit all participants whilst accelerating innovation.

Consider how Moderna developed its COVID-19 vaccine: leveraging a network including the NIH for research, commercial manufacturers for scale-up, and government programmes for distribution. This achievement would have been impossible under traditional pharmaceutical development models.

A networked approach offers access to best-in-class capabilities regardless of organisational size, parallel processing accelerating timelines, and increased resilience through redundancy. Pharma leaders will win not by owning every capability, but by orchestrating and integrating the best that the R&D ecosystem has to offer. This coordination has been enabled by technological advances that are dismantling traditional competitive moats and creating new sources of advantage based on data integration and computational capability.

Data and technology enablers

The shift from monolithic pharmaceutical companies to networked ecosystems is fundamentally enabled by technology's democratisation of capabilities once exclusive to big pharma. When Deep 6 AI identifies trial candidates "in minutes, not months" across 25 million patient records, and Komodo Health provides insights from 330 million patient journeys, scale advantages evaporate. The AI pharmaceutical market, growing from US$ 1.94 billion in 2025 to US$ 16.49 billion by 2034 (27 per cent CAGR), is not just accelerating existing processes, it is removing fundamental constraints. Insilico Medicine's progression from target discovery to Phase 2 trials in under 30 months (versus 6-7 years traditionally) exemplifies how AI is reimagining development itself. AlphaFold's 200 million freely available protein structures eliminate the need for a whole team of researchers, letting startups begin where big pharma would have spent years arriving.

This democratisation creates a strategic paradox: if everyone has access to the same AI platforms, such as Amgen with NVIDIA, and J&J/Novo Nordisk/Grifols sharing Cradle Bio, where is competitive advantage? The answer: data sovereignty. Whilst computational capabilities commoditise, proprietary datasets remain unique. With health data expanding 36 per cent annually, differentiation comes from generating, curating, and integrating comprehensive datasets — clinical trials, real-world outcomes, preclinical successes, failed experiments, biomarker correlations. According to Accenture, companies must allocate 8-10 per cent of R&D budgets to digital initiatives to merely remain relevant. Those who successfully build integrated, interoperable data infrastructure, with AI embedded throughout their R&D platforms position themselves to maximise the value of technology partners moving forward. However, the path to achieving this integration varies significantly depending on organisational context.

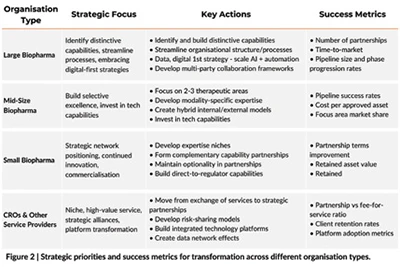

Strategic adaptations for success in the ecosystem era

The ecosystem paradigm creates new strategic imperatives that differ fundamentally between company types. Successful transformation requires tailored strategies leveraging existing strengths whilst building new capabilities.

Risks and mitigation strategies

The ecosystem model introduces vulnerabilities; success in the ecosystem era also requires robust risk mitigation strategies:

As these capabilities become table stakes, the pharmaceutical landscape of 2030 will be shaped by those moving beyond defensive governance to offensive value creation.

Looking ahead to 2030

The pharmaceutical R&D landscape of 2030 will feature radical departures from today's practices:

• The exponential impacts of AI, transforming how decisions are made, and work is done, and providing accurate predictions, driving faster and better outcomes

• AI-powered drug discovery, real-world evidence platforms, clinical trial optimisation tools, and advanced analytics capabilities available today through specialised technology providers are only the beginning

• Deeper understanding of human biology, thanks to data and computing power

• Empowered patients and new value pool created around the consumer

• Continuous evidence generation using digital health technologies

• Decentralised manufacturing with on-demand production

• New participants including patient advocacy groups and technology companies in prominent roles

• Organisational agility as a key differentiator

Conclusion

The pharmaceutical industry's evolution from integrated companies through the BIPCO model toward networked ecosystems represents natural progression driven by technological advancement and economic realities.

This transformation offers significant opportunities: access to world-class capabilities regardless of organisational size, faster development through parallel processing, and increased innovation through coordination of diverse specialties. Success will belong to organisations that master network orchestration, leverage data as their primary differentiator, and build flexible partnership models that capture value across multiple nodes.

The future of pharmaceutical innovation lies not in controlling all aspects of drug development, but in effectively orchestrating the remarkable capabilities emerging across the global R&D ecosystem. The true measure of this transformation will be how quickly breakthrough medicines reach patients who desperately need them. The ecosystem built today determines the therapies delivered tomorrow.

Biopharma leaders are faced with a decision: drive this transformation or be driven out by it.

References:

Bleys, M., Khan, B., Wu, J. and Chandran, P. (2025). Biopharma Trends 2025: Focusing on Innovation amid Complexity. Boston Consulting Group (BCG), 8 January. Available at: https://www.bcg.com/publications/2025/biopharma-trends [Accessed 26 September 2025].

Deloitte (2024). Unleash AI's potential: Measuring the return from pharmaceutical innovation (14th edition). Deloitte LLP, April 2024. Available at: https://www2.deloitte.com/uk/en/pages/life-sciences-and-healthcare/articles/companies-have-reversed-the-decline-in-the-returns-from-pharma-r-and-d.html [Accessed 27 September 2025].

Dunleavy, K. and Sagonowsky, E. (2025). ‘2024 drug approvals: Small companies loom large with several key FDA nods’. FiercePharma, 28 January. Available at: https://www.fiercepharma.com/pharma/2024-drug-approvals [Accessed 26 September 2025].

IQVIA (2024). Global Trends in R&D 2024: Activity, productivity, and enablers. IQVIA Institute, 22 February 2024. Available at: https://www.iqvia.com/insights/the-iqvia-institute/reports-and-publications/reports/global-trends-in-r-and-d-2024-activity-productivity-and-enablers [Accessed 26 September 2025].

Lehmann, T., Paraggio, N., Swarna, K., Karaca-Griffin, S. and Blumberg, A. (2024). Reinventing R&D in the age of AI: How intelligent technologies are transforming the Biopharma Industry. Accenture. Available at: https://www.accenture.com/content/dam/accenture/final/accenture-com/document-2/Reinventing-RandD-In-The-Age-Of-AI-Report.pdf [Accessed 28 September 2025].

McKinsey (2025b). Simplification for success: Rewiring the biopharma operating model. McKinsey Life Sciences Practice, March 2025. Available at: https://www.mckinsey.com/industries/life-sciences/our-insights/simplification-for-success-rewiring-the-biopharma-operating-model [Accessed 26 September 2025].

Author Bio

Lavinia Woodward holds a First-Class Honours degree in Medical Sciences from the University of Oxford and has built her career at the intersection of scientific complexity and commercial strategy, developing data and technology solutions for complex drug development challenges. Currently, she leads the Client Advisory and Consulting function at Excelra, bridging the gap between scientific data and decision-grade intelligence.