The Middle Eastern pharmaceutical market is undergoing an unmatched transformation, fuelled by robust economic initiatives, ambitious healthcare reforms, and strategic government investments. The pharmaceutical market in the Gulf Cooperation Council (GCC) region has an annual revenue of around US$17 billion; projected to grow annually (CAGR 2025-2029) by nearly 5 per cent, market volume will reach US$21.5 billion by 2029. This remarkable growth trajectory positions the region as a prime destination for global pharmaceutical companies seeking expansion.

Government -backed programmes, such as the UAE’s US$1.3 billion healthcare allocation and Saudi Arabia’s Vision 2030, are setting the stage for significant advancements. These initiatives, with the overarching goal of diversification of the economy away from oil, focus on localising manufacturing, fostering innovation, and improving access to healthcare. Combined with favourable demographics, rising healthcare expenditures, and increasing prevalence of chronic diseases, the Middle East is rapidly becoming a global hub for pharmaceutical growth (Figure 1).

Market evolution and opportunities

The Middle East is increasingly recognised as a centre for cutting-edge pharmaceutical innovation and research. From leveraging artificial intelligence (AI) to facilitating advanced clinical trials, the region is transforming its healthcare landscape.

Rapid growth trajectory

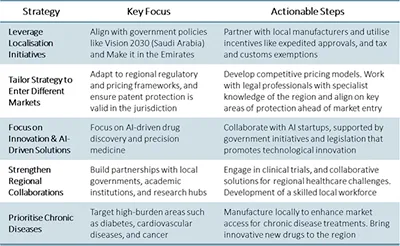

The Middle East’s pharmaceutical market growth outpaces many mature markets, with healthcare spending comprising up to 5.4 per cent of the UAE’s GDP in 2024 and growing at a compound annual growth rate (CAGR) of 8.5 per cent. The rising prevalence of chronic diseases, particularly diabetes and hypertension, drives significant demand for innovative and cost-effective therapies. Nearly 70 per cent of deaths in the Gulf Cooperation Council (GCC) are attributable to non-communicable diseases (NCDs), with this figure reaching 78 per cent in Saudi Arabia. This underscores the critical need for investments in preventive care and treatment options.

Manufacturing localisation and partnerships

Despite heavy reliance on imported pharmaceuticals, the Middle East is steadily advancing local manufacturing capabilities. Saudi Arabia’s Vision 2030 prioritises reducing dependence on imports by investing in technology transfer and incentivising domestic production. Public-private partnerships present lucrative opportunities for multinational firms to localise production, transfer expertise, and capitalise on burgeoning demand. This progress unfolds against a backdrop of government initiatives, which expedite approval for locally produced therapies, and provide tax, customs, and repricing regulations exemptions.

The region is actively investing in enhancing biopharma manufacturing capabilities, as exemplified in the following partnership. Following the receipt of multiple rounds of equity financing from Abu Dhabi’s state-owned Mubadala Investment Company in the early 2020s, US-based manufacturer National Resilience entered a partnership with the sovereign investor in 2023. Mubadala was to construct a manufacturing facility in Abu Dhabi, which would be operated by National Resilience, producing advanced biopharmaceuticals. This will be the first Goods Manufacturing Practice (GMP) manufacturing facility in the UAE.

Demographic drivers

The region’s unique demographic profile is a key driver of pharmaceutical demand. A young and increasingly affluent population drives the need for preventive care and vaccines, while an ageing demographic generates demand for chronic disease management solutions. Additionally, a growing middle class with higher disposable income has further accelerated healthcare expenditure.

Strategic advantages

The Middle East is rapidly emerging as a strategic focal point for the pharmaceutical industry. This transformation is underpinned by a confluence of advantages, including advanced clinical research infrastructure, strong geopolitical connectivity, and numerous economic incentives tailored to attract global investment.

Advanced clinical research ecosystem

The Middle East is also establishing itself as a hub for advanced clinical trials. Streamlined regulatory processes in countries like Saudi Arabia enable faster trial approvals, reducing the time-to-market for new drugs. Furthermore, the region’s genetically diverse populations offer unique opportunities for developing tailored therapies. High-tech facilities equipped with advanced diagnostics and monitoring tools enhance the precision and efficiency of clinical trials.

Geopolitical and logistic benefits

The Middle East’s strategic location at the crossroads of Europe, Asia, and Africa provides unparalleled connectivity for pharmaceutical distribution. State-of-the-art infrastructure, including advanced cold-chain logistics and emerging high-capacity manufacturing facilities, ensures seamless operations across the pharmaceutical value chain. Additionally, innovations in digital health and telemedicine further augment the region’s capabilities. A growing number of the large pharma players are establishing regional hubs, tapping into the UAE’s highly connected logistics network, ensuring efficient delivery of medicines across the Middle East and North Africa, and beyond, thereby enhancing their market presence.

Infrastructure gaps

Despite considerable investments in local manufacturing, infrastructure gaps remain a significant challenge. Many countries still rely heavily on imports to meet domestic pharmaceutical demand, which presents an opportunity for multinational pharmaceutical companies to step in. By leveraging technology transfers, forming international partnerships, and investing in manufacturing capabilities, these firms can not only address supply shortages but also establish a strong market presence. This approach aligns with the region’s goals of achieving self-sufficiency and reducing costs and offers large pharma companies long-term growth potential in a rapidly expanding market.

Economic incentives

Governments across the region offer an array of economic incentives to attract multinational pharmaceutical companies. These include tax-free operations in specialised zones, such as the Dubai Science Park (where all the top 10 biopharma companies have offices), expedited registration processes, and 100 per cent foreign ownership in key sectors. Free land and low-cost electricity and water are also being offered to boost its profile as an attractive destination for global investors and position itself as a global hub of innovation.

Challenges and solutions

The Middle East's rapid pharmaceutical growth is accompanied by distinct hurdles that companies must navigate.

Regulatory fragmentation

In the Middle East, fragmented and often less transparent regulatory frameworks present a key difficulty for international pharmaceutical businesses. Patent protection is also a challenge, as securing intellectual property rights in one jurisdiction does not guarantee coverage in others. This multi-jurisdictional complexity can drive up costs and increase uncertainty, particularly when entering markets with varying foreign direct investment rules.

Solution: Tailoring strategies to each country and working with experienced legal teams with specialist knowledge of the region can help companies to navigate these regulatory and patent challenges and mitigate the associated risks.

Cost pressures

While the region offers opportunities for growth, healthcare budgets in some countries are constrained. Governments often prioritise cost-effective solutions, posing challenges for expensive advanced therapies.

Solution: Focusing on affordability through biosimilars, generics, and valuebased pricing models can improve market access. Collaborating with governments on public–private partnerships can also reduce financial barriers.

Skilled workforce

As the Middle East’s pharmaceutical sector expands, the demand for highly skilled professionals in areas such as research, manufacturing, and clinical trials is outpacing the available talent pool. Fostering a local specialised pharmaceutical workforce will be crucial to build a sustainable industry ecosystem.

Solution: Partnerships between multinational pharmaceutical companies and local universities to create training programs to equip students and professionals with the expertise needed to sustain growth.

Success Stories and Market Entry Models

Recent moves by global biopharmaceutical companies demonstrate diverse and successful approaches to establishing and expanding presence in the Middle Eastern market. These case studies offer valuable insights into effective market entry strategies and partnership models.

Strategic partnerships

The collaboration between California-based BridgeBio Pharma and the UAE’s Burjeel Holdings exemplifies the region's commitment to bringing innovative solutions to the region. Their partnership, centred in Abu Dhabi, leverages the Emirate's advanced infrastructure for conducting clinical trials and Burjeel’s foundation in healthcare delivery and outreach, with BridgeBio’s established expertise in creating transformative therapies for genetic diseases. The project, known as NADER (Needs Assessment and Therapeutics for Rare Diseases — ‘nader’ meaning ‘rare’ in Arabic), focuses on the early diagnosis and treatment of rare genetic diseases in the UAE. It is worth noting that BridgeBio also received US$250 million private placement equity financing led by the Qatar Investment Authority (QIA) in 2023.

Manufacturing localization

Sanofi's recent partnership with Saudi Arabian drugmakers Arabio and Lifera demonstrates successful manufacturing localisation, in line with Saudi Arabia's Vision 2030 goal of a more self-sufficient healthcare ecosystem. The collaboration focuses on producing seven vaccines included in Saudi Arabia's mandatory immunisation schedule, utilising Lifera as a contract manufacturer and planning the buildout of a new manufacturing facility. Arabio will utilise its local and regional distribution capabilities to support the supply of vaccines and other biopharmaceutical products to the Saudi market. This setup supports the ongoing effort of pharmaceutical localisation in the Middle East, while granting Sanofi enhanced market access.

Similarly, AstraZeneca, with its Gulf headquarters located in the Dubai Science Park, entered a strategic partnership agreement with Abu Dhabi’s AI-powered healthcare company, G42 Healthcare at the end of 2022, outlining a multi-year comprehensive process to manufacture innovative drugs in Abu Dhabi. This builds on the Declaration of Collaboration made by the two companies a year earlier, to enhance clinical research and diagnostics frameworks in the UAE.

Research and development hubs

The establishment of Insilico Medicine's Generative AI and Quantum Computing Research and Development Centre in Abu Dhabi marks the region's largest AI-powered biotechnology research centre. Located within the International Renewable Energy Agency (IRENA) headquarters in Masdar City, a hub of sustainability and innovation, the centre benefits from the Middle East’s AI laws, which foster a relaxed regulatory environment conducive to experimentation and rapid development. This strategic positioning enables the centre to pioneer advanced solutions for rare diseases, ageing, and sustainable chemistry, and supports the digital transformation of healthcare in the region.

To navigate challenges and capitalise on the Middle East’s opportunities, pharmaceutical companies must adopt targeted strategies:

Distribution networks

Virax Biolabs' strategic decision to establish regional headquarters in Dubai Science Park demonstrates how companies can leverage the UAE's position as a gateway to broader markets. By entering the region, Virax Biolab aims to increase its distribution reach of high-quality in-vitro diagnostics and proprietary T-Cell tests, while creating logistical efficiencies. In line with the Dubai Economic Agenda 'D33', the new headquarters will create new jobs and drive talent to the UAE, while also enhancing healthcare in the region.

Conclusion

With its proactive government support, advanced infrastructure, and a burgeoning ecosystem of innovation, the Middle East presents a unique and lucrative opportunity for big pharma. Challenges, including regulatory harmonisation and workforce development, remain. Success in the region requires long-term investment, strong local partnerships, and alignment with regional healthcare needs. By capitalising on these opportunities, the Middle East is poised to become a central hub for global pharmaceutical expansion.

References

1) Healthark Insights. "Market Access for Pharma and Medical Devices in MENA Region." Healthark Insights, https://healtharkinsights.com/access-blog/market-access-for-pharma-and-medical-devices-in-mena-region. Accessed 13 Jan. 2025

2) Simmons & Simmons. Health Horizons: Opportunities Emerge as Sectors Converge. Simmons & Simmons, 2024.

3) Research and Markets. "Middle East Clinical Trials Market." Research and Markets, https://www.researchandmarkets.com/report/middle-east-clinical-trials-market?utm_source=BW&utm_medium=PressRelease&utm_code=ddkmvp&utm_campaign=2020467+-+GCC+Pharmaceutical+Market+Opportunity+%26+Clinical+Trials+Outlook+Report+2030+-++A+More+Than+US%2412+Billion+Market+Opportunity+By+2030&utm_exec=carimspi. Accessed 14 Jan. 2025.

4) JLL. "Enhancing Resilience in GCC Pharma and Biotech Through R&D." JLL, https://www.us.jll.com/en/trends-and-insights/investor/enhancing-resilience-in-gcc-pharma-and-biotech-through-r-and-d#:~:text=The%20Gulf%20Cooperation%20Council%20%28GCC%29%20is%20on%20the,to%208%25%2C%20the%20region%20is%20ripe%20for%20innovation. Accessed 14 Jan. 2025.